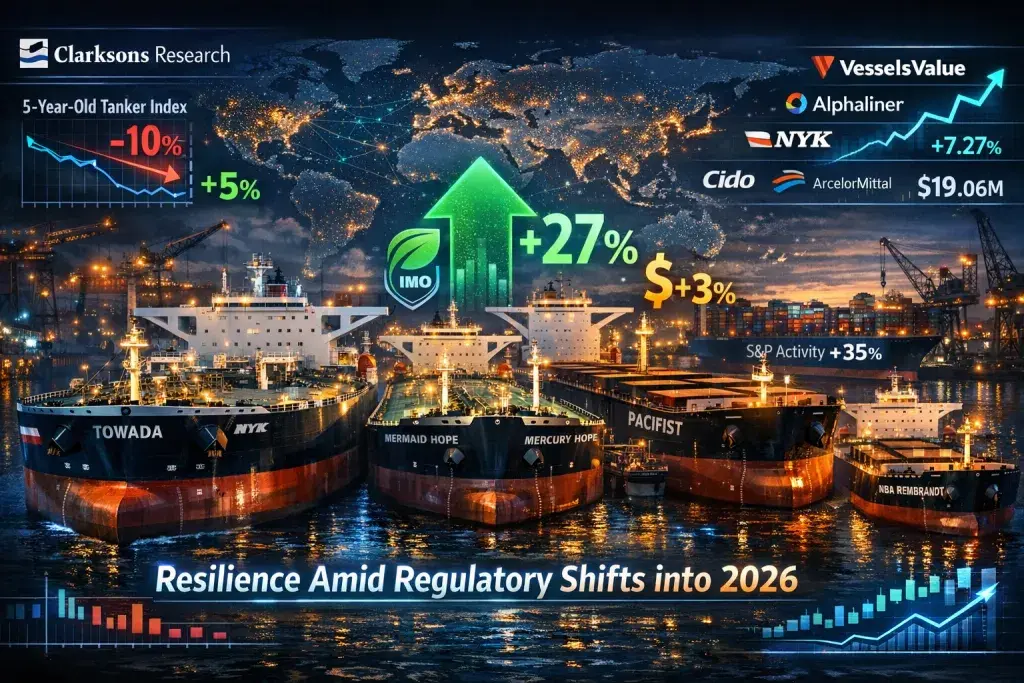

In the first part of 2025, tanker sale and purchase (S&P) activity has shown robust health, with Clarksons Research logging 409 tankers totaling 44.5 million dwt and $13.9 billion in value sold so far—a 27% increase in deadweight tonnage over the 2024 run rate, though only 3% up in dollars amid declining secondhand prices. This resilience signals sustained investor confidence in the sector despite pricing headwinds.

Tanker Market Leads with Volume Gains

Clarksons’ five-year-old tanker secondhand price index averaged 10% lower in 2025 than 2024, yet ticked up 5% since September, reflecting stabilizing demand. VesselsValue data highlights December stability across sectors, with VLCCs posting the strongest gains: 20-year-old 310,000 dwt units rose 7.27% month-on-month to $43.21 million, driven by tight supply of compliant vessels amid environmental regulations.

- Key deals: NYK sold the 19-year-old VLCC Towada for $45.7 million.

- Cido Shipping offloaded the 14-year-old VLCCs Mermaid Hope and Mercury Hope en bloc for $120 million.

These transactions underscore a preference for older tonnage, as buyers capitalize on availability shortages for eco-compliant ships, potentially fueling fleet modernization pressures.

Bulkers Lag in Volume but Values Climb

Bulker S&P has been subdued, with just 14 carriers traded in early December despite firm freight and charter rates. Values held steady, led by capesizes: 20-year-old 180,000 dwt vessels gained 5.42% to $19.06 million.

- NGM Shipping flipped the 14-year-old Japanese-built Pacifist cape from $19 million five years ago to $32 million, highlighting lucrative capital gains.

- NYK Bulkship sold the 2012-built 107,000 dwt NBA Rembrandt for $18.7 million to ArcelorMittal Shipping, following its sistership NBA Rubens at $15 million.

Strong fundamentals suggest selective buying, with older assets benefiting from elevated rates and scarcity.

Containers Hold Firm Amid Divergent Trends

Container S&P mirrors a stable charter market, up 35% year-over-year against 2024 averages, per Alphaliner, even as spot 40ft rates plunged 45%. Demand persists for mid-sized tonnage.

- En bloc sale of 8,568 teu sisters Cypress, Koi, and Lotus A to Global Ship Lease for $90 million, with time charter back to CMA CGM.

“Sale and purchase is ending 2025 cheerfully, with firm prices across sizes,” Alphaliner noted, pointing to structural demand outweighing freight volatility.

Outlook: Resilience Amid Regulatory Shifts

Healthy tanker volumes despite softer pricing reflect broader shipping trends: geopolitical tensions boosting ton-mile demand, IMO regulations tightening compliant supply, and opportunistic plays yielding gains. Expect continued activity into 2026, as values stabilize and buyers target assets bridging the green transition gap, bolstering sector liquidity.