Indiana finds itself in an increasingly awkward position: one of the most restrictive cannabis regimes in the country, surrounded by states that have moved to adult-use legalization and a federal government edging toward rescheduling. Two new reports from RAND, commissioned by the Richard M. Fairbanks Foundation, put concrete numbers to what many already suspected - that prohibition, in practice, has not kept cannabis out of Hoosier hands. It has simply redirected where the money goes and who captures the regulatory oversight.

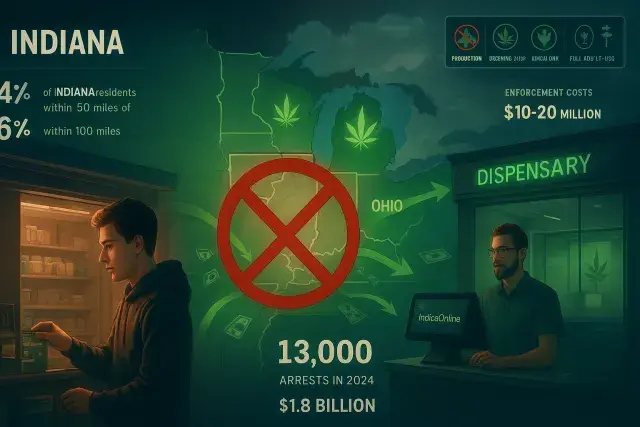

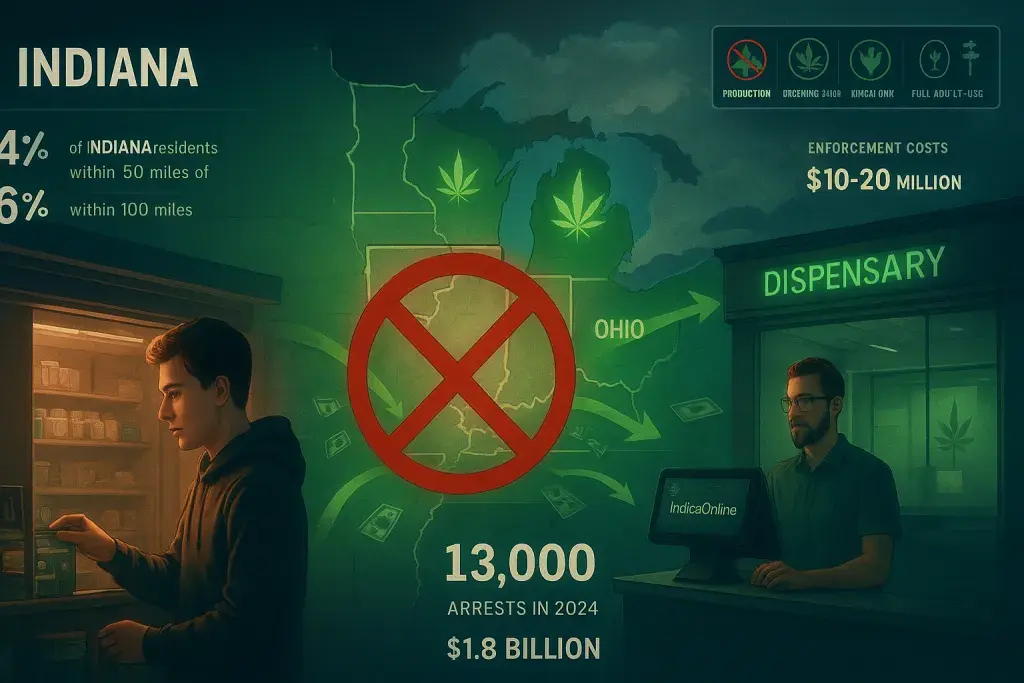

According to the RAND research, 44 percent of Indiana residents live within 50 miles of a licensed dispensary in a neighboring state, and 96 percent live within 100 miles. That is not a policy victory for prohibition; it is a market reality. Operators in Illinois, Michigan, and Ohio are already running sophisticated licensed retail operations - complete with seed-to-sale tracking, age-verified transactions, and compliant packaging - that serve Indiana consumers every day. Those dispensaries rely on point-of-sale infrastructure like IndicaOnline cannabis POS to manage inventory, maintain compliance logs, and process transactions within their own states' regulatory frameworks, the kind of operational discipline Indiana's own market, if it ever materializes, would need to replicate from day one. Meanwhile, Indiana collects none of the excise tax revenue, employs none of the compliance infrastructure, and bears none of the regulatory responsibility for those sales.

There is a second, less-discussed pressure point: intoxicating hemp products. Delta-8 THC and similar hemp-derived compounds - which can carry the same psychoactive effects as conventional marijuana - are sold openly at gas stations, grocery stores, and convenience stores across Indiana, with limited oversight and no meaningful age-gate enforcement at point of sale. These products exist in a regulatory gray zone created by the 2018 federal Farm Bill's definition of hemp, and Indiana has not moved aggressively to close it. The practical result is that a 17-year-old can potentially access an intoxicating hemp product at a corner store while the state spends enforcement resources on adult marijuana possession charges.

What the Numbers Actually Say About Costs and Revenue

The RAND estimates are worth sitting with, because they correct a common overstatement in legalization debates. Annual state revenue from adult-use cannabis legalization is estimated at approximately $180 million - real money, but roughly 1 percent of Indiana's general fund. For comparison, cigarette and alcohol taxes combined brought in $385 million in 2025, according to the Indiana Department of Revenue. Cannabis is not a budget solution. Anyone selling it as one is overpromising.

On the cost side, Indiana recorded over 13,000 cannabis-related arrests in 2024. More than 90 percent were for possession; more than 75 percent were connected to non-cannabis charges - meaning cannabis enforcement is often a secondary action attached to other police contact, not a stand-alone priority. The state spends an estimated $10 million to $20 million annually on cannabis law enforcement. Legalization would reduce some of that expenditure, but not eliminate it. A regulated adult-use market carries its own ongoing regulatory costs - licensing administration, lab testing oversight, market surveillance, illicit market enforcement - that RAND estimates could run into the low tens of millions annually. The net fiscal math is tighter than advocates often admit.

Cannabis use in Indiana has more than doubled over the past decade, with growth especially pronounced among adults 26 and over. RAND estimates 1.3 million Hoosiers used cannabis in 2024, spending approximately $1.8 billion on marijuana products. That spending currently flows out of state or into unlicensed markets. Neither outcome generates Indiana tax revenue, and neither carries consumer safety protections - no lab testing requirements, no certificate of analysis, no compliant packaging standards, no dosage disclosure.

The Policy Menu - and Why the Tradeoffs Are Genuine

The RAND reports do not advocate for a particular outcome. That restraint is worth respecting. The options they describe range from maintaining full prohibition to decriminalization, medical-only legalization, or a full adult-use market - each carrying distinct tradeoffs across public health, criminal justice, state revenue, and market structure.

For B2B operators watching from neighboring states or positioning for a potential Indiana market, the 14 policy design considerations RAND identifies matter enormously. License caps, vertical integration rules, excise tax rates, social equity provisions, home delivery authorization, consumption lounge allowances - each decision reshapes the economics for operators, wholesalers, and brands before a single product ever hits a shelf. States that set excise taxes too high relative to neighboring markets have watched illicit and gray-market sales persist because licensed retail cannot compete on price. States that restricted vertical integration created supply chain friction that slowed market launches. Indiana's leaders, if they move toward any form of regulated market, would be choosing not just a policy framework but an entire retail and compliance architecture.

The persistence of intoxicating hemp products adds another layer. Any Indiana regulatory framework that does not address delta-8 and similar compounds alongside marijuana policy will have a structural gap on day one. Retailers in licensed markets in other states deal with this constantly - consumers who arrive comparing hemp-derived products bought locally against regulated cannabis flower, with no consistent understanding of potency, dosage, or sourcing across those product categories.

What Operators and Industry Watchers Should Track

Indiana is not moving fast. But the conditions that typically precede policy shifts are present: neighboring state legalization creating cross-border market pressure, growing use rates, mounting enforcement costs with arguable public safety returns, and a federal rescheduling conversation that could change the legal backdrop for every state still in the prohibition column.

For multi-state operators, real estate investors, cannabis software vendors, compliance consultants, and wholesale brands, Indiana represents a watch-list market - not an imminent opportunity, but one that warrants serious preparation. If legalization does come, the state's political culture suggests it would likely favor a cautious market structure: limited initial licenses, conservative excise tax design, strict product testing requirements, and a medical program as a possible precursor to adult-use. That is speculation, to be clear. But it is informed speculation based on how similar states have approached the sequence.

The most useful thing Indiana's policymakers could do right now - whatever direction they ultimately move - is to treat the RAND research as a baseline, not a conclusion. The decisions made at the drafting stage of cannabis regulation are extraordinarily hard to unwind. States that designed their markets poorly in the early years of legalization are still paying for those choices in suppressed tax revenue, persistent illicit markets, and compliance systems that were retrofitted rather than built right. Indiana has the advantage of going later. Whether it uses that advantage is the actual question.